Scientists discover rare genetic condition that attacks kids’ immune systems

2 Biotech Stocks That Are Screaming Buys This Month

They won't remain southbound forever.

CRISPR Therapeutics (CRSP 3.22%) and Moderna (MRNA 2.57%) have much in common. They're both innovative biotechs working in relatively newer niches of this booming industry.

However, they've moved in the wrong direction this year. CRISPR's shares are down by 27% year to date, and Moderna's are down by 41%. Regardless of their performances so far in 2024, both stocks are worth investing in this month. Read on to find out why.

1. CRISPR TherapeuticsCRISPR Therapeutics recently hit a breakthrough point when it earned approval for its first product, Casgevy, a therapy for sickle cell disease and transfusion-dependent beta-thalassemia. Casgevy is also the first medicine on the market that uses the famous CRISPR gene editing technique. Given this significant milestone, why is the company underperforming the market?

Here are two potential reasons. First, after Casgevy's approval, some investors decided to take some profits. Second, it will take time before Casgevy contributes meaningfully to CRISPR Therapeutics' financial results. Ex vivo gene editing medicines like Casgevy require that patients' cells be collected and used to manufacture the treatment before it's reinserted into them. The process takes a while and can only be done in qualified treatment centers.

Though it's impossible to ignore these factors, investors may be undervaluing Casgevy's prospects. CRISPR Therapeutics partnered with biotech giant Vertex Pharmaceuticals to develop and market it. As a result, the medicine earned approval in places a midcap biotech by itself may not have targeted: Saudi Arabia and Bahrain. These markets alone have some 23,000 eligible patients. The partners estimate an addressable market of 35,000 people in the U.S. And Europe.

Casgevy, at a price of $2.2 million in the U.S. -- and very little competition to speak of, at least for now -- could easily vastly exceed the $1 billion in sales milestone. Yes, it might take a little longer than it would if Casgevy were an oral pill, but patient investors should bide their time.

That's why CRISPR Therapeutics is a great stock to buy this month. It hasn't performed well this year, but over the long run, it has the tools to become a major player in the promising gene editing realm. Interested investors should scoop up the company's shares while they're down.

2. ModernaModerna made a name for itself during the pandemic by developing and marketing a successful COVID-19 vaccine. Although sales from this product have fallen off a cliff, the company has made plenty of progress.

Moderna is setting a solid foundation that could allow it to perform well over the long run. That starts with newer approvals: Moderna has now earned the green light for an RSV vaccine called mRESVIA and should launch at least one other product within the next couple of years.

The company's combined coronavirus/flu vaccine aced a phase 3 study. It elicited higher immune responses than some individual vaccines in both categories in its late-stage trial.

Few people like getting shots, even if it's necessary to do so. Getting one beats getting two, provided patients don't have to sacrifice efficacy. It looks like that won't be a problem.

Moderna has several other phase 3 candidates -- a potential stand-alone flu vaccine, one for the cytomegalovirus (there currently is none), another for the norovirus, and still another that's being developed as a personalized cancer vaccine in collaboration with Merck. Moderna should recover in time, even of its financial results currently don't inspire confidence.

What does that mean for investors? The stock is down 41% year to date. There are several potential catalysts related to the company's late-stage pipeline on the horizon that could jolt the stock price.

In the long run, Moderna's vast pipeline of mRNA-based products should help it develop plenty of successful candidates. Now is a good time to buy.

Prosper Junior Bakiny has positions in Vertex Pharmaceuticals. The Motley Fool has positions in and recommends CRISPR Therapeutics, Merck, and Vertex Pharmaceuticals. The Motley Fool recommends Moderna. The Motley Fool has a disclosure policy.

This Healthcare Growth Stock Could Be A Steal Of A Deal Right Now

CRISPR Therapeutics is trading around multiyear lows.

Finding an undervalued growth stock can lead to some oversize returns in the long run. In some cases, it can be as simple as focusing on sectors of the market that might not be getting much attention of late, and thus could make for attractive under-the-radar investments right now.

One stock that has been struggling and that arguably should be doing a lot better these days is CRISPR Therapeutics (CRSP 3.22%). There was a lot of excitement around the healthcare company early on in the year, but over the past six months, its shares have crashed by more than 30%. Here's why I think it could be a bargain right now.

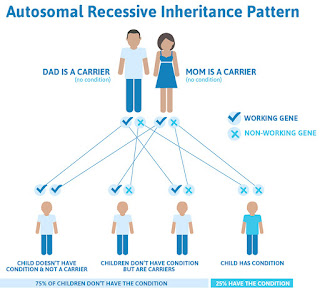

CRISPR's future looks more promising than everLast year, the Food and Drug Administration (FDA) granted approval for CRISPR's gene therapy for sickle cell disease for patients who are 12 years and older. Casgevy is a one-time treatment that, even priced at more than $2 million, is cost-effective for the patient and their insurer, according to the Institute for Clinical and Economic Review.

CRISPR has been developing the treatment along with its partner Vertex Pharmaceuticals, with CRISPR taking a 40% share of profits on the treatment. In January, the FDA also approved Casgevy for transfusion-dependent beta thalassemia, also in patients who are 12 and older.

As a result of the approvals, optimism was high around CRISPR at the beginning of the year, only for that bullishness to eventually wane. The two companies, CRISPR and Vertex, are still in the early stages of rolling out Casgevy, however, so it will take time before investors start to see a financial boost from the approvals.

At its peak, Casgevy could generate $3.6 billion in revenue. CRISPR will only share in the profits on that, but given the high price tag, it could still represent a significant amount for the company, and it might be enough for it to get out of the red. In its most recent quarter, which ended on June 30, the company incurred a net loss of $126.4 million. Now that Casgevy is approved for not just one but two indications, there could at least be a path to profitability in the future.

CRISPR is also working on developing other therapies to bolster its portfolio even further, including CTX211 as a possible treatment for type 1 diabetes.

The stock could be overdue for a big rallyAccording to analyst price targets, the upside for CRISPR's stock could be as high as 66%. And those targets are just based on where analysts think the stock can go in the short term (i.E., 12 months). In the long run, there could be even more room for the share price to go higher.

Given that CRISPR has a couple of approvals and is a well-funded company with over $2 billion in cash and marketable securities on its books as of the end of June, this isn't nearly as risky as other biotech stocks.

What I suspect has happened is that investors have truly just forgotten and overlooked CRISPR because the focus for much of the year has been on companies involved in artificial intelligence. Although CRISPR did have some positive news at the beginning of the year, that might not have been enough to keep investors' attention, and that's evident with a sharp reduction in trading volume.

CRSP 30-day average daily volume; data by YCharts.

As CRISPR starts to post some stronger financials resulting from Casgevy, I would expect to see some excitement and bullishness return to the stock, and I think that's simply a question of when it will happen -- and not if.

Should you buy CRISPR Therapeutics stock?CRISPR is trading around the levels it was at five years ago, and yet the business is in much better shape than it was back then. Although it could take some time for its financials to benefit from Casgevy's rollout, the company seems to be on a much better path today than it was five years ago. For the stock to be trading at these levels looks to be a great opportunity to lock in a good price for one of the safer, more promising biotechs in the market today.

As long as you're willing to be patient, CRISPR Therapeutics could make for a fantastic buy right now.

David Jagielski has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends CRISPR Therapeutics and Vertex Pharmaceuticals. The Motley Fool has a disclosure policy.

Got $1,000? 2 Magnificent Growth Stocks To Buy And Hold Forever

Many growth stocks have experienced pressure over the last few years as investor sentiment has shifted amid the changing macroeconomic backdrop. While no one can predict what the market will do next, if you're investing for five, 10, or 15 years in quality businesses, near-term market movements shouldn't deter you from putting cash to work.

If you're looking for top growth stocks to add to your portfolio right now, here are two names to consider for your buy list.

1. Vertex PharmaceuticalsVertex Pharmaceuticals (NASDAQ: VRTX) has grown into a veritable giant over the last decade with its leadership in the cystic fibrosis therapeutics market. The company bears the distinction of being the only name in the industry with drugs approved that treat the root genetic cause of this disease. In fact, one of the linchpins in Vertex's business strategy is focusing on rare diseases or underserved disease areas for which there are minimal to no viable treatment options and developing treatments that target the root cause of these conditions.

The most recent approval for Vertex was Casgevy, the product of a long-standing partnership with CRISPR Therapeutics. Not only is Casgevy designed to be a one-time functional cure for both sickle cell disease (SCD) and transfusion-dependent beta thalassemia (TDT), but it was also the first CRISPR therapy approved in history.

Because Casgevy is a gene-editing therapy, administration is a lengthy and highly involved process. Patients must prep to have their blood stem cells collected for around two months, and once they are collected, editing the cells for reinfusion takes anywhere from five to six months. Then, the patient must undergo chemotherapy before they can receive Casgevy, after which there is a recovery period.

Beyond the timeline to administer Casgvey, the therapy's $2.2 million price tag brings unique considerations for payers, so Vertex's ability to execute solid reimbursement agreements with public and private payers will be key. Vertex has actively been working alongside payers to achieve this goal. For example, in August, the company announced that it had reached a reimbursement agreement with England's National Health Service for eligible TDT patients to receive Casgevy.

While momentum from the gene-editing therapy will take time to manifest on the top and bottom lines, analysts think that Casgevy will bring in an additional $3 billion or more annually for Vertex in the future.

Beyond recent developments with Casgevy, Vertex has been going from strength to strength in other areas. It's awaiting approval for a new triple-combination cystic fibrosis therapy that could be even more effective than its existing flagship therapy, Trikafta. The company is also working on securing the regulatory green light for suzetrigine, its non-opioid drug for moderate to severe acute pain. Suzetrigine is also being studied as a treatment for diabetic peripheral neuropathy.

Story continues

These are likely to be the two most near-term launches, but Vertex is also developing a stem-cell therapy designed to target the underlying cause of Type 1 diabetes, and drugs that target the root genetic causes of APOL1-mediated kidney disease (AMKD), myotonic dystrophy type 1 (DM1), and autosomal dominant polycystic kidney disease (ADPKD).

In the second quarter, Vertex reported product revenue of $2.65 billion, up 6% from the prior year period. The company has historically been very profitable, but its recent acquisition of Alpine Immune Sciences (a biotech that develops novel protein-based cancer immunotherapies), pushed its bottom line into the red in the three-month period. That should be a short-term phenomenon.

This follows the first quarter of 2024, in which it reported revenue of $2.69 billion, up 13% from one year ago, while net income popped 57% year over year to $1.1 billion.

Vertex looks like it's on a robust growth trajectory built on a solid foundation from its existing leadership in the cystic fibrosis space, and that's a growth story healthcare investors might want to capitalize on sooner rather than later.

2. Palantir TechnologiesPalantir Technologies (NYSE: PLTR) builds and leverages software platforms that help government and commercial enterprises review, integrate, synthesize, and streamline data.

The big data analytics company originally focused on members of the intelligence community, but it's been slowly but surely diversifying its revenue streams to large public and private companies. Palantir's client base is diverse. It ranges from companies like United Airlines and Ferrari to the United States intelligence community and the Department of Defense. Its core products include Gotham, Foundry, Apollo, and its Artificial Intelligence Platform (AIP).

Gotham has historically been used by members of the U.S. And international intelligence communities to centralize intelligence gathering and drive better decision making across countless use cases, whether in planning missions, targeting enemies, or other military operations. Foundry helps corporate clients manage and analyze data to transform workflow processes, while Apollo helps to manage and utilize software that controls Palantir's various products in the cloud.

Palantir only launched its AIP in 2023, but it's already experienced rapid adoption among government and commercial clients to employ AI-driven decision making in real time.

AIP has been a major driver of Palantir's recent successes and appears to be increasingly integral to the company's long-term growth story. Not only have new customers been drawn to AIP, but many of Palantir's existing customers have added AIP to their long-term agreements with the company. Chief Revenue Officer Ryan Taylor gave some notable examples of the success of AIP with existing customers on the Q2 earnings call:

Tampa General signed a seven-year expansion, deploying AIP to deliver a care coordination operating system, where we've helped them reduce patient length of stay by 30%. Panasonic Energy of North America signed a three-year expansion using AIP across finance, quality control, and manufacturing operations.

AARP shared they're utilizing AIP to provide targeted, personalized experiences for their 29 million unique visitors on a monthly basis. Eaton deepened our relationship, leveraging AIP to modernize ERP deployments in addition to finance, sales, and supply chain use cases. Kinder Morgan signed a five-year Foundry and AIP enterprise expansion with production use cases, including storage optimization, pipeline integrity monitoring, and power optimization.

Palantir is now in the process of launching its latest product, called Warp Speed. Chief Technology Officer Shyam Sankar said that Warp Speed is designed "to power American reindustrialization" and was envisioned as "an operating system for the modern American manufacturer." Sankar said that the new back-end platform is built on AIP with industrial AI and was formulated from years of helping industrial customers build everything from automobiles to planes.

For the second quarter of 2024, the company generated $678 million in revenue, up 27% year over year. Government revenue totaled $371 million, while commercial revenue came in at $307 million. Those figures were up 23% and 33%, respectively, from one year ago. Palantir closed 27 deals worth over $10 million in business revenue in the three-month period alone, while its customer count jumped 41% from one year ago. Profits for the three-month period totaled $134 million, although Palantir has brought in net income of about $405 million over the last 12 months.

The stock's on a winning streak right now, but the long-term picture for this business looks even more enticing for investors.

Should you invest $1,000 in Vertex Pharmaceuticals right now?Before you buy stock in Vertex Pharmaceuticals, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Vertex Pharmaceuticals wasn't one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... If you invested $1,000 at the time of our recommendation, you'd have $826,069!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of October 7, 2024

Rachel Warren has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends CRISPR Therapeutics, Kinder Morgan, Palantir Technologies, and Vertex Pharmaceuticals. The Motley Fool has a disclosure policy.

Got $1,000? 2 Magnificent Growth Stocks to Buy and Hold Forever was originally published by The Motley Fool

View comments

Comments

Post a Comment